When you log into a Peer-to-Peer (P2P) lending platform, the experience is incredibly smooth. You deposit funds, set up an auto-invest strategy, and watch as your dashboard updates daily with fractional interest payments. It feels almost like magic, or at least like a highly efficient savings account.

But P2P platforms are not banks, and your money isn’t just sitting in a vault generating yield out of thin air.

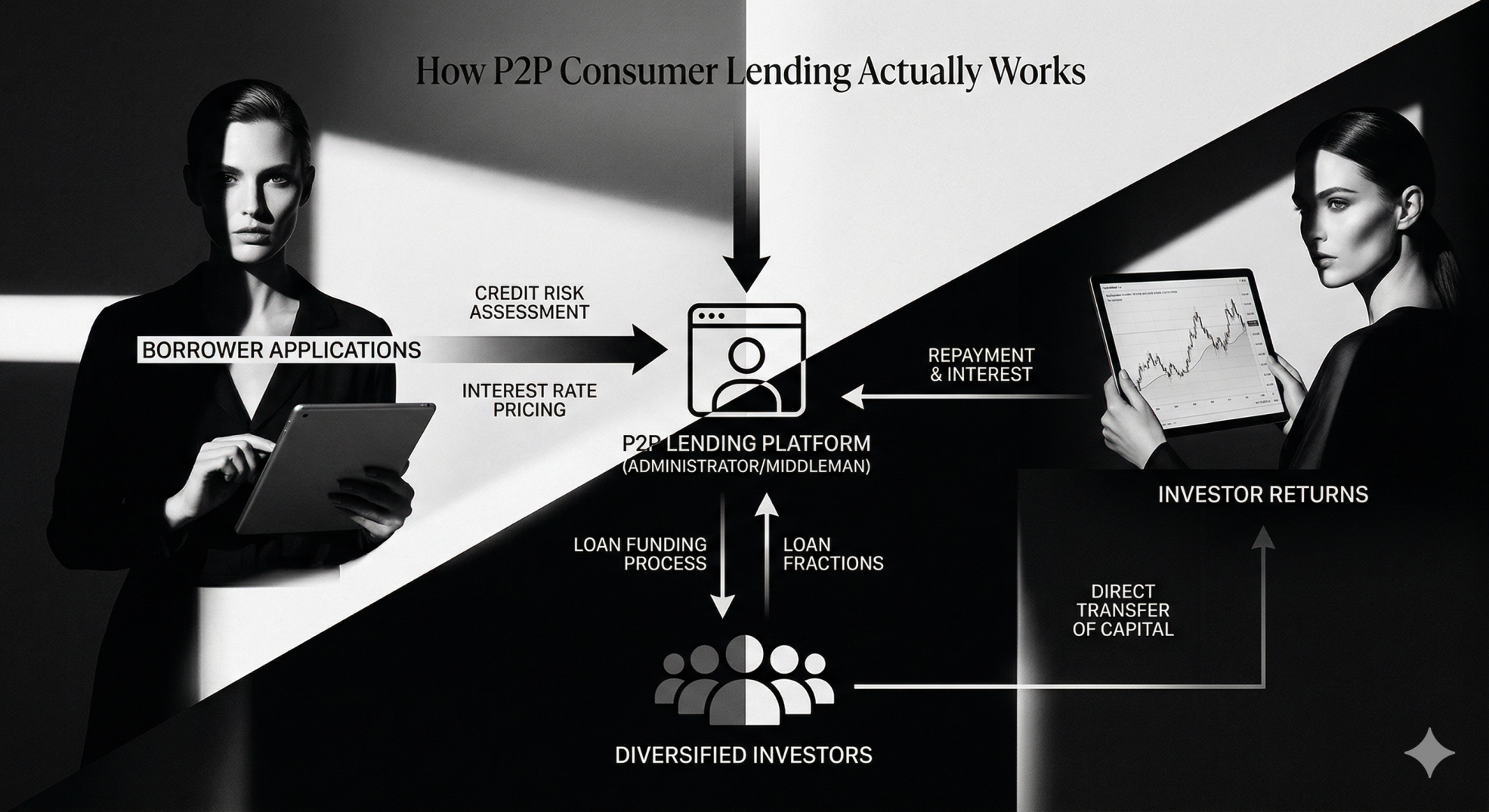

If you are going to invest your hard-earned money into consumer loans, you need to know exactly where it goes once it leaves your digital wallet. Here is a look behind the curtain at the real mechanics of P2P consumer lending.

The Three Main Players

To understand the background process, you first need to understand that modern P2P investing (often called marketplace lending) usually involves three distinct parties:

- The Borrower: An everyday person looking for a personal loan, a car loan, or short-term consumer credit to buy a new appliance.

- The Loan Originator (Lending Company): The local financial institution in the borrower’s country that actually evaluates the borrower, approves the loan, and issues the money.

- The P2P Platform: The online marketplace (like Lendermarket, Mintos, or Peerberry) that connects the Loan Originators with retail investors like you.

Step-by-Step: The Journey of Your Investment

So, how does a borrower in Spain buying a new laptop turn into a 10% yield on your dashboard? Here is the lifecycle of a P2P consumer loan.

Step 1: Origination and “Skin in the Game”

The process actually starts before you ever see the loan. A borrower applies for credit with a local Loan Originator. The Originator runs a credit check and approves the loan.

Crucially, the Originator issues the loan using their own capital first. To ensure they don’t just approve terrible loans and pass the risk onto you, platforms require Originators to keep a percentage of the loan (usually 5% to 10%) on their own balance sheet. This is called having “skin in the game.”

Step 2: Fractionalization and Listing

Once the loan is issued to the borrower, the Originator wants to free up their capital so they can issue more loans.

They take that loan and list the remaining 90% to 95% on the P2P Platform. The platform then “fractionalizes” the loan—chopping a €2,000 car loan into tiny €10 pieces.

Step 3: You Fund the Loan

Your auto-invest tool kicks in. It takes €10 from your account and buys one of those fractions.

Where does your €10 go? It goes directly to the Loan Originator. You are essentially reimbursing the Originator for the money they already lent out. In exchange, you acquire the right to receive the future interest and principal payments tied to that specific €10 fraction.

Step 4: The Repayment Flow

A month later, the borrower pays their monthly installment to the local Loan Originator.

The Originator keeps a small cut for servicing the loan and passes the rest of the interest and principal to the P2P Platform. The platform’s software instantly calculates your exact share and deposits the micro-cents of interest into your investor account.

The Safety Net: How Buyback Obligations Work

In the world of consumer loans, borrowers default. It is an unavoidable statistical reality. So, why doesn’t your portfolio constantly show negative returns?

The secret mechanism running in the background is the Buyback Obligation (sometimes called a Buyback Guarantee).

- If the borrower is more than 60 days late on their payment, the Loan Originator is contractually obligated to step in.

- The Originator uses their own corporate profits to buy the bad loan back from you, paying you your full principal plus the accrued interest.

- The Originator then handles the messy, time-consuming debt collection process locally, while your capital is freed up to invest in a new, performing loan.

The Catch: This means your true risk is not really the individual borrower defaulting; your true risk is the Loan Originator going bankrupt. If the lending company fails, the buyback obligation vanishes, and you are left holding fractions of defaulted consumer loans.

The Bottom Line

The smooth, passive income you see on your dashboard is the result of a highly active, cross-border financial machine.

By understanding that your money is flowing to Loan Originators to fund actual consumer credit, you can make smarter decisions. You aren’t just trusting the P2P platform’s interface; you are relying on the financial health and underwriting standards of the lending companies behind the scenes.

Discuss this article / 0 comments